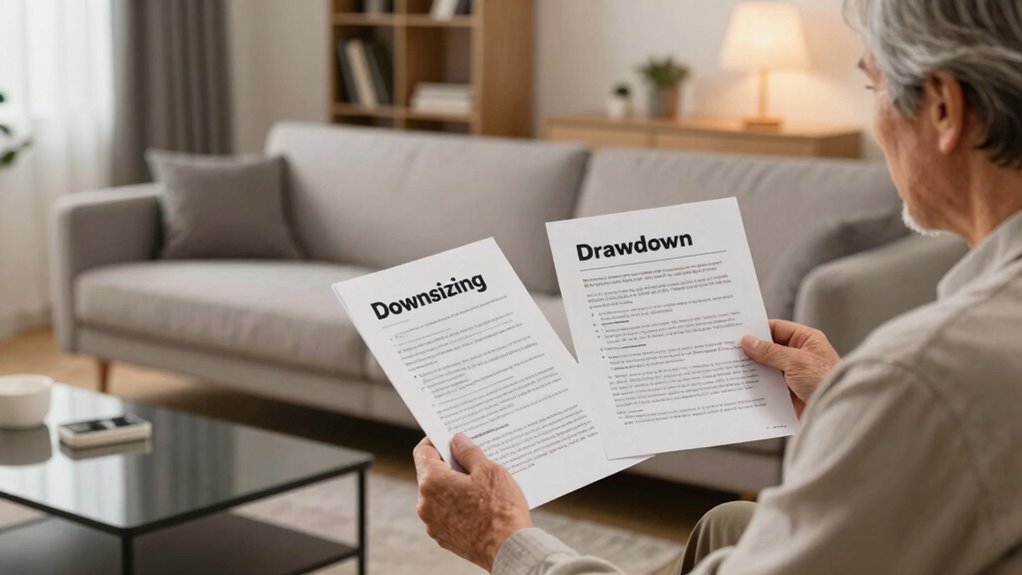

Choosing between downsizing and a drawdown lifetime mortgage can greatly impact your finances and inheritance. Downsizing involves selling your home for a smaller property, potentially reducing your estate, while a drawdown mortgage lets you access home equity without moving, but interest accumulates over time. Both options offer benefits and drawbacks, so understanding these differences is essential to avoid costly mistakes. Keep exploring to discover more about how to make the best choice for your future.

Key Takeaways

- Downsizing involves selling your home for cash and moving to a smaller property, while a drawdown lifetime mortgage allows borrowing against your current home without moving.

- Downsizing reduces property ownership and inheritance potential; a drawdown mortgage retains ownership, affecting estate value differently.

- Drawdown mortgage interest accrues over time, potentially decreasing your estate, whereas downsizing provides immediate cash but may limit future wealth.

- Downsizing simplifies decision-making but involves relocation; drawdown mortgages are more complex with ongoing interest costs.

- Your choice depends on priorities like maintaining estate inheritance versus accessing flexible retirement funds.

Are you contemplating ways to access the equity in your home to support your retirement plans? If so, you’re likely exploring options that can boost your income or provide funds for future needs. Two popular choices are downsizing and drawdown lifetime mortgages. While both can help you tap into your home’s value, understanding their differences is essential to avoid costly mistakes that could impact your retirement planning and estate inheritance.

Downsizing involves selling your current home and purchasing a smaller, often more manageable property. This move can free up significant cash, reduce maintenance costs, and sometimes lower property taxes. It’s a straightforward way to access your home’s equity, giving you a lump sum or regular income to support your lifestyle or cover unexpected expenses. Downsizing can be especially appealing if your current home no longer suits your needs or if you want to simplify your life. However, it’s vital to consider how this decision affects your estate inheritance. Selling your home means you’re transferring ownership, which could reduce the assets you pass down to heirs. If leaving an estate is a priority, you’ll need to weigh the benefits of extra cash now against the potential decrease in inheritance.

Selling your home to downsize can free cash but may reduce the inheritance you leave behind.

On the other hand, a drawdown lifetime mortgage allows you to stay in your home while borrowing against its value. You retain ownership but take out a loan that grows over time, with interest added. You can access funds as needed, either as a lump sum or regular payments. This option can be advantageous if you want to preserve your property’s value for inheritance or prefer not to move. It offers flexibility, helping you manage your retirement income more effectively without immediate upheaval. Yet, a drawdown mortgage can be more complex, with interest accruing over time, potentially reducing the estate you leave behind. It’s important to understand the interest accumulation process when considering this option. If estate inheritance is a priority, you’ll need to plan carefully, considering how the loan might impact your beneficiaries. Additionally, understanding holistic wellness principles can help you approach your financial decisions with a balanced perspective, ensuring your choices support both your physical and financial health. Being aware of financial implications can further assist in making well-informed decisions that align with your overall retirement strategy. Moreover, considering biodiversity and sustainability practices can also influence your long-term planning, encouraging choices that support your values and environmental impact. Recognizing the importance of financial planning can also help you navigate the complexities of these options more effectively, ensuring your decisions are aligned with your future goals.

home equity drawdown lifetime mortgage

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

Can I Switch Between Downsizing and Drawdown Mortgages Later?

Yes, you can switch between downsizing and drawdown mortgages later, but it depends on your lender’s policies. First, you’ll need a property valuation to assess your current home’s worth and consider moving costs involved in downsizing. Switching might involve fees or penalties, so it’s wise to consult your lender early. Planning ahead helps guarantee the change aligns with your financial goals and avoids unexpected expenses.

Are There Any Tax Implications With Each Mortgage Type?

You’ll find that downsizing often offers tax advantages, such as freeing up cash to invest or pay off debts, but it might impact inheritance considerations, as you may need to sell your property. Drawdown mortgages typically don’t trigger immediate tax implications, though the proceeds could affect your estate. Always consult a financial advisor to understand how each mortgage type could influence your taxes and inheritance plans, ensuring you make the best choice.

How Do Interest Rates Differ Between Downsizing and Drawdown Options?

You’ll find that interest rate comparison for downsizing and drawdown options often shows drawdown mortgages offering more flexible rates, which can be advantageous if mortgage rate fluctuations occur. Downsizing mortgages may have fixed rates, providing stability. However, drawdowns typically adjust with market changes, so if rates drop, your costs could decrease. Understanding these differences helps you choose a plan aligned with your financial goals and the current interest rate environment.

What Are the Eligibility Criteria for Each Mortgage Type?

You might wonder if you qualify for these options. To be eligible, your property value needs to meet specific thresholds—usually, your home must be worth enough to secure the loan. For downsizing, you need to plan to move to a smaller property, while drawdown requires you to be of a certain age, often over 55. Loan eligibility depends on your financial situation, property value, and age, so check these carefully before deciding.

Do Both Options Affect My Estate Planning Equally?

Both options impact your estate planning differently. A downsizing mortgage may free up assets and alter your inheritance planning, potentially increasing your estate’s value. In contrast, a drawdown mortgage keeps your property intact but reduces your estate’s total valuation, affecting inheritance plans. You should consider how each affects your estate valuation and inheritance goals, ensuring your choices align with your long-term estate planning objectives.

Downsizing & Decluttering for Seniors Made Simple: Large Print Guide to Simplify Your Household, Let Go of Belongings after Retirement & Prepare for a Peaceful Move to a Smaller Home

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

Choosing between downsizing and a drawdown lifetime mortgage is like steering a winding river—you need to pick the right vessel to reach your destination safely. Each option has its own currents and eddies, and a small mistake could lead to costly surprises. By understanding their differences, you’re guiding your financial ship with confidence, avoiding treacherous waters. So, weigh your options carefully—because the right choice can be the anchor that keeps your future secure and steady.

Equity Release and Retirement: Your Guide to Later Life Mortgage Options

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Warning Sign Retiree Permanent On Site Vintage Private Property Novelty Plaque Rust Free Aluminum 8×12 Inch Sturdy Wall Plaque For Cabin Farm Garage Yard Indoor Outdoor

Core Dual Function :8×12 6×8 and 12×16, 4×16 inch Multi-Size Vintage Aluminum Warning Sign, Retro Safety Decor |…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.