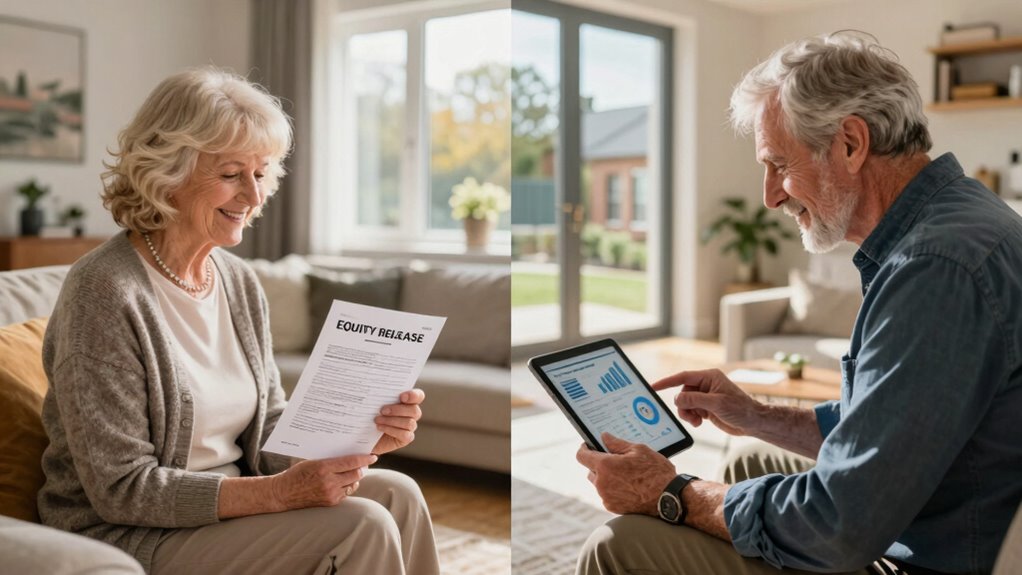

If you’re considering opening up your home’s equity, it’s essential to understand the differences between reverse mortgages and equity release schemes in the UK and US. Reverse mortgages don’t require monthly payments and are mainly for older homeowners, while equity release includes options like lifetime mortgages and home reversion, offering more flexibility but involving selling part or all of your home. Making the right choice can save you from costly mistakes—discover more to make informed decisions.

Key Takeaways

- Reverse mortgages are primarily for older homeowners to access tax-free income without monthly repayments, mainly in the US, while equity release in the UK includes various schemes for broader purposes.

- Both schemes depend on property valuation, but reverse mortgages loan based on home equity, with interest accruing over time, whereas equity release options may involve selling part of the home or exchanging ownership rights.

- UK and US regulations differ significantly, affecting scheme protections, costs, and eligibility, making understanding local legal safeguards essential.

- Costs such as fees, interest, and early repayment charges vary, impacting long-term estate value and inheritance plans.

- Choosing the right scheme requires understanding individual financial goals and potential penalties to avoid costly mistakes.

When considering ways to access your home’s equity, understanding the differences between reverse mortgages and equity release schemes is essential, especially in the UK and US markets. Both options allow homeowners to tap into their property’s value, but they serve different purposes and come with distinct implications. If you’re thinking about your retirement planning, knowing these differences can help you avoid costly mistakes and make informed decisions.

Understanding the differences between reverse mortgages and equity release is crucial for smart retirement planning.

A reverse mortgage generally targets older homeowners who want to supplement their income during retirement. It allows you to borrow against your property’s value without monthly repayments, as the loan is repaid when you sell the home or pass away. The key here is the property valuation—lenders assess your home’s worth to determine how much you can borrow. This scheme can be a valuable part of your retirement planning if you need extra cash but want to stay in your home. However, it’s important to understand that interest on the loan accrues over time, which can reduce your estate’s value and potentially impact inheritance plans.

Equity release schemes, often more flexible, include options like lifetime mortgages and home reversion plans. While they also enable you to unlock equity from your property, they are generally used for a broader range of purposes, including funding home improvements, paying off existing debts, or supporting family members. Equity release products tend to have different terms and conditions, and some may involve selling a portion of your home or exchanging ownership rights. When considering these options, you need to carefully evaluate how they fit into your overall retirement planning and lifestyle goals.

In both the UK and US, the process begins with a professional property valuation to accurately determine your home’s current market value. This step is crucial because it influences the amount you can borrow and the long-term impact on your estate. Additionally, understanding the regulations and protections in place can help you navigate potential risks more confidently. You should also consider the costs involved, including fees, interest rates, and any early repayment charges, which can vary significantly between schemes and regions.

Ultimately, your choice between a reverse mortgage and an equity release scheme depends on your specific financial situation, retirement goals, and how you want to manage your property. Making the wrong decision could cost you dearly—either by reducing your home’s value prematurely or limiting your flexibility in the future. Taking the time to understand each option thoroughly ensures you select the best approach for your circumstances, helping you secure your retirement without unexpected surprises.

Reverse Mortgages: Elements, Considerations and Market Developments (Housing Issues, Laws and Programs)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

Can I Qualify for Both Reverse Mortgage and Equity Release Simultaneously?

You generally can’t qualify for both a reverse mortgage and equity release simultaneously, especially due to restrictions on joint applications. Lenders usually prevent loan overlap to protect your financial stability. If you’re considering both options, it’s best to consult a financial advisor who can guide you on the right approach. Combining these loans often isn’t allowed, so exploring alternative strategies might be necessary to meet your goals.

How Do Interest Rates Compare Between UK and US Options?

Interest rate comparison shows US reverse mortgages often have slightly higher rates than UK equity release plans, mainly due to different loan structures. In the US, interest rates typically range from 3% to 5%, with variable or fixed options. UK equity release rates tend to be lower, averaging around 3% to 4%. Loan term differences influence these rates: US loans usually span 10-15 years, while UK plans often last until death or move.

Are There Age Restrictions for Each Type of Loan?

You need to meet specific age restrictions for each loan type. For UK equity release, you typically must be at least 55, while in the US, reverse mortgages usually require you to be 62 or older. Loan eligibility depends on your age, home value, and financial situation. These age restrictions guarantee you’re eligible to access your home’s equity, so check the specific requirements for your location before applying.

What Happens if I Outlive My Loan Term?

If you outlive your loan term, you typically have repayment options like selling your property or using inheritance planning strategies. Some loans may offer a ‘roll-up’ feature, allowing the debt to grow until the property is sold or inherited. It’s essential to understand these options to avoid unexpected costs and guarantee your estate remains intact for your heirs. Always review the terms carefully before choosing a loan to match your long-term plans.

Do These Options Affect Eligibility for Government Benefits?

Yes, reverse mortgages and equity release can affect your eligibility for government benefits. These options may impact your eligibility criteria, especially for means-tested benefits like Pension Credit or Housing Benefit. It’s important to check how the lump sum or monthly payments might influence your benefits. Consulting a financial advisor helps make certain you understand these effects and avoid unintentionally losing crucial support.

Driving Customer Equity : How Customer Lifetime Value is Reshaping Corporate Strategy

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

Understanding the difference between reverse mortgages and equity release isn’t just about choosing a financial product; it’s about making a decision that impacts your future, your security, and your peace of mind. Know what suits your needs, understand the risks, and ask questions. Because when you’re informed, you’re empowered. When you’re empowered, you make the right choice. And when you make the right choice, you secure your future, protect your home, and preserve your peace of mind.

The Man Who Knew: The Life and Times of Alan Greenspan

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

ASURION 3 Year Home Improvement Protection Plan ($250 – $299.99)

- No Extra Cost for Repairs: Parts, labor, and shipping included

- Comprehensive Coverage: Drops, spills, cracks, and surges covered

- Immediate Claims Process: Online or phone claims, quick approvals

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.